Lincoln Financial Long-Term Disability Denials

Lincoln Financial is a large insurance company headquartered in Pennsylvania, and it’s worth almost $400 billion in total assets. They offer both short- and long-term disability (LTD) benefits. Lincoln Financial offers ERISA-governed group policies, so you may have a claim with them through your employer.

You may also have a claim with Lincoln Financial if you had a claim with Liberty Mutual. This is due to Lincoln Financial having bought out Liberty Mutual’s disability insurance operations. If this is the case, Lincoln Financial now handles your Liberty Mutual claim.

Nonetheless, developing a medical condition that prevents you from working can qualify you for LTD benefits. Lincoln Financial denies claims frequently, however. This article will discuss Lincoln Financial, why it may deny your LTD claim, how to appeal their decision, and more.

Why Does Lincoln Financial Deny Long-Term Disability Claims?

Lincoln Financial sends LTD claimants a denial letter when it denies a claim. This letter cites the reasons behind their decision. They may deny a claim for several reasons, including:

- Lack of evidence

- Failing to meet the applicable definition of disability

- Surveillance tactics inject doubt into a claim

- Independent medical exam results counter the claim

- Missing deadlines

- And more

Your Lincoln Financial LTD insurance policy will have a definition of disability. This will either be an “own” or an “any occupation” definition. All claimants must prove their disability meets this definition to receive benefits or risk a denial of their claim. Read our in-depth article on the definition of disability for more information.

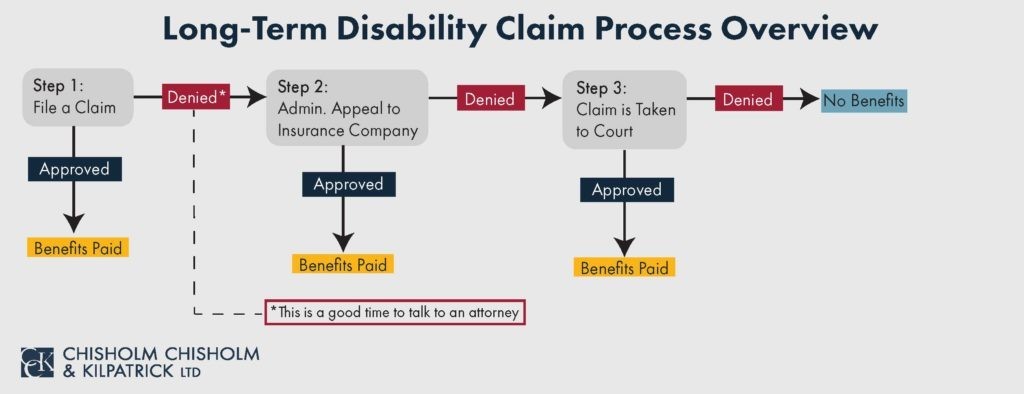

How to File a Long-Term Disability Appeal with Lincoln Financial

Facing a denial of an initial claim can be overwhelming, but all claimants have the right to file an administrative appeal. The appeal stage is a crucial part of the process of getting disability benefits because under ERISA, it is often the last time to submit new and submitted evidence.

All claimants should thoroughly read their Lincoln Financial denial letter. As mentioned, it will list the specific reasons why they denied the claim. Claimants should directly address these reasons in their appeal.

For example, if Lincoln Financial cites a “lack of evidence” in the denial letter, then claimants should submit additional evidence to refute this in the appeal.

Supplemental evidence, while not always necessary, can help reinforce a claim. This evidence can include:

- Specialized reports from treating physicians

- Additional medical tests, such as MRIs and X-rays

- Functional capacity evaluations

- Witness statements

- Vocational evaluations

- And more

Nevertheless, Lincoln Financial does not want to approve LTD claims if it can help it and they will try and find reasons to deny a person’s appeal. Consequently, this is why many claimants choose to utilize a long-term disability lawyer during this stage.

Obstacles LTD Claimants May Encounter When Filing an Appeal

It should be a straightforward process to obtain LTD benefits but this is not always the reality claimants face. Insurance companies like Lincoln Financial do not want to pay claims, so they will try and find reasons to deny them. As such, claimants may encounter several obstacles when filing an appeal.

These obstacles can include:

- Surveillance tactics: Lincoln Financial may employ surveillance tactics as they did during the initial claim. They may surveil claimants to try and unearth a discrepancy in their claim/appeal.

- Social media monitoring: As with in-person surveillance, Lincoln Financial may also monitor a claimant’s social media platforms. Insurers can take a photograph or post from the claimant out of context and use it to deny their appeal.

- Independent medical exams: Often, insurers request claimants attend an IME. However, these medical evaluations are often performed by a doctor paid for by the insurance company. Thus, these “independent” exams are often biased against the claimant and can lead to a denial of benefits.

- Decision delays: Lincoln Financial may take decision deadlines extensions to delay the claim. Under ERISA, they can take a 45-day extension if they believe a claimant did not submit enough information for them to make a decision.

Obstacles like these can derail a claim. All claimants who receive a denial of their appeal should check the terms of their policy. There may be more appeals available to them. If not, they have the right to file a lawsuit to get their benefits.

Call CCK Law Today

Handling an appeal on your own can be stressful. Luckily, it’s not something you must handle on your own. It’s easy to make common mistakes, but CCK Law can help you avoid them and strengthen your claim.

Our team is prepared to help you with your Lincoln Financial long-term disability appeal. We can act as a point of contact between you and Lincoln Financial, can collect and submit all evidence on your behalf, keep track of all deadlines, and more.

Call us today at (800) 544-9144 for a free case evaluation with a member of our team. We will analyze your case and determine if we can assist.

Share this Graphic