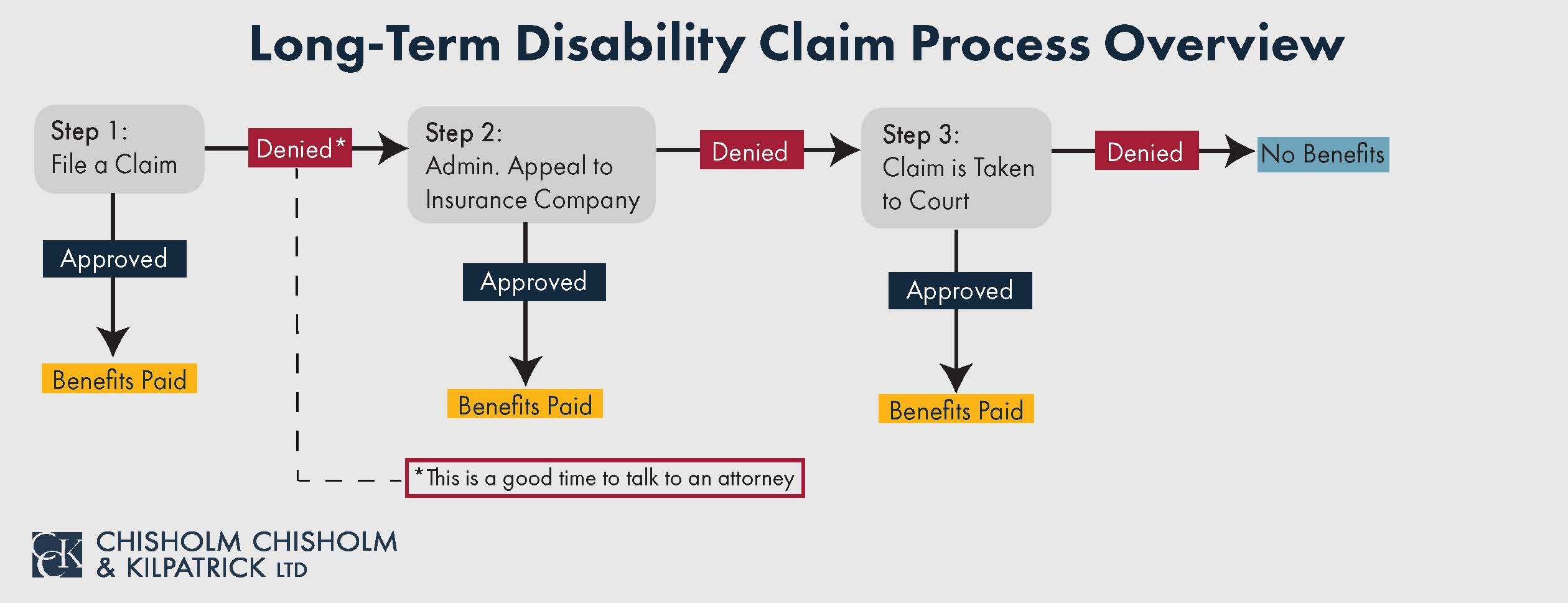

What Is a Social Security Offset for Long-Term Disability?

If you are disabled and are no longer able to work, you may be able to receive long-term disability (LTD) benefits. You receive these benefits if you can meet the definition of disability outlined in your policy. These benefits will cover a percentage of your pre-disability income. However, there are often provisions under many long-term disability policies that allow for the reduction of your benefits based on your other sources of income. This deduction is known as an offset. One major offset of long-term disability benefits is Social Security Disability Insurance (SSDI) benefits.

What are Social Security Benefits?

Long-term disability policies, including those governed by ERISA, often require you to apply for Social Security disability benefits. Social Security disability benefits are government-funded disability benefits, as opposed to long-term disability benefits, which you receive through an insurance provider. You are eligible for Social Security benefits if you have paid Social Security taxes on your work earnings, have worked for a certain amount of time, and meet their definition of total disability.

Why Does My Long-Term Disability Insurance Company Require Me to Apply for SSDI?

Your long-term disability policy will likely require you to apply for Social Security disability benefits. If you are approved, your insurance company can offset your long-term disability benefit with the amount you receive for SSDI. This saves the insurance company money and ensures you are not double-dipping in multiple benefits.

While it is free to apply for Social Security Disability Insurance, approval can be difficult. SSDI has strict requirements, and it can be difficult to meet its definition of total disability. If you are denied, your long-term disability policy may require you to exhaust your appeals. Not applying for or appealing a denial of SSDI can be cause for your long-term disability insurance company to deny you LTD benefits.

How Do Long-Term Disability and Social Security Benefits Work Together?

If it is free to apply for SSDI, why bother with the premiums for long-term disability insurance? Social Security Disability Insurance requires total disability, which can be a difficult definition of disability to meet, and SSDI is often more stringent than long-term disability policies. And if you are approved, payments for Social Security Disability Insurance are often lower than those from long-term disability insurance.

Even if your long-term disability payments are offset by SSDI, you will likely get more income coverage under both than under Social Security Disability Insurance alone. It is also important to note that the approval period for Social Security benefits can be lengthy, and long-term disability benefits can cover you during this approval period.

Be Aware of How Your SSDI Offset is Affecting Your Long-Term Disability Payments

If you are approved for Social Security Disability Insurance, you will want to pay attention to how your insurance company begins to offset your long-term disability benefits. You may want to review your policy to be aware of how Social Security Disability Insurance works within your specific plan, or make sure that your insurance company is calculating your offset correctly. Taking such precautions can ensure that you are not wrongfully losing money.

It is also important to be aware of the legal ways Social Security Disability Insurance can lower your long-term disability payments. One potential occurrence to be aware of is double offsets. Sometimes, individuals are covered under two or more long-term disability policies. If both policies provided for an offset of SSDI benefits, it could result in a double offset, and you may receive less disability income than planned.

For example, if you had two long-term disability policies that each paid $2,000 per month, you would expect $4,000 of monthly disability income. If each policy provides for a Social Security Disability Insurance offset, and your SSDI benefit was $1,000 per month, courts have ruled that the insurer may take an SSDI offset from both policies, thus, the insured is left with $3,000 in monthly disability income–$1,000 from each LTD policy, and $1,000 from SSDI.

Contact the Attorneys at Chisholm Chisholm & Kilpatrick Today

Filing a claim for long-term disability benefits can be challenging, especially with potential SSDI offsets. However, this is not something individuals must handle on their own. A long-term disability lawyer can help LTD claimants maneuver the complexities of the claim process. If you’re having trouble navigating your offsets or believe your insurance company is wrongly offsetting your benefits, you can reach out to CCK Law.

For over 25 years, our team has been helping long-term disability claimants get the benefits they need, and we may be able to help you, too. Call us today at (800) 544-9144 for a free case evaluation.

Share this Graphic