Going from Short-Term Disability to Long-Term Disability

Short-term disability (STD) insurance provides financial benefits when you become temporarily disabled and cannot work. This type of insurance typically covers conditions such as temporary injuries, surgery rehabilitation, and pregnancy. On the other hand, long-term disability (LTD) insurance provides financial benefits if you become disabled and are unable to work for a longer period.

Typically, for short-term disability coverage to begin, you must be unable to work for a certain period—usually one or two weeks. Short-term disability usually lasts for about three to six months of coverage. Conversely, long-term disability insurance requires you to be disabled for 90 to 180 days before the benefits begin; after that, benefits can last for a certain number of years or until you reach retirement age.

Short-term disability insurance also provides benefits to cover the waiting period before long-term disability benefits begin. If you receive the maximum amount of short-term disability benefits allowed under your policy, you may need to transition to long-term disability benefits.

STD and LTD insurance are often offered as part of your employment benefits, but you can also purchase them directly from an insurance company. You do not need to have both types of disability coverage from the same insurance company, though it may make transitioning between the two easier.

Differences Between STD and LTD Definitions of Disability

Although they provide similar benefits, there are often differences between STD and LTD plans. The most important difference is the definition of disability that you need to meet under the two policies. Short-term disability policies usually require you to meet an “own occupation” definition, which means that you must be unable to perform the duties of your specific job. The definition of disability usually remains the same during your claim. Moreover, STD policies often require that you receive appropriate treatment during the duration of your disability.

Long-term disability, however, can be either an “own occupation” or an “any occupation” definition of disability. The “any occupation” definition means that you must be unable to perform the duties of any job whatsoever in order to continue receiving benefits. Usually, after 24 to 48 months of an “own occupation” definition, LTD policies will transition to the “any occupation” definition.

Limitations in Long-Term Disability Policies

Long-term disability policies are often more restrictive than short-term disability policies. For example, LTD policies often have restrictions that can limit the types of conditions that may be approved for benefits or limit how long you will receive benefits for certain conditions.

Certain disabilities are covered by your STD policy but not your LTD policy. For example, if you recently obtained both policies and became disabled due to a condition that existed prior to getting the coverage, your long-term disability most likely will not cover it. This is because most LTD coverage excludes preexisting conditions.

Therefore, it is best to not assume that because you were approved for short-term disability that you will also be approved for long-term disability.

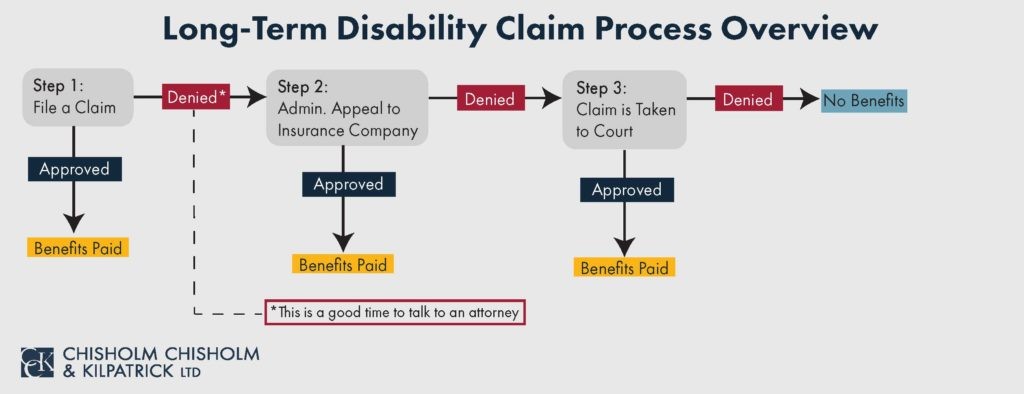

If you are having difficulty reading and understanding the terms of your policies, a long-term disability lawyer can help. Moreover, if you are transitioning from one policy to the other, an attorney will be best equipped to guide you through the process.

Transitioning from STD to LTD with the Same Insurance Company

Transitioning from short-term to long-term disability may be easier for those whose long-term disability coverage is provided by the same insurance company that handled their short-term disability claim. This is because an insurance company that already covered you for STD benefits will have already found you disabled. Further, they will typically already have a substantial amount of your medical records and/or reports from your providers supporting your claim.

Often in those cases, the insurance company will evaluate your claim for long-term disability benefits before your short-term disability benefits end to eliminate the need to go through a new claim process. However, you may still need to complete some claim paperwork.

It is important that your LTD claim is consistent with what you reported during your STD claim. It is also important to be aware that, even though your short and long-term policies may be from the same insurance company, each plan likely has different eligibility requirements. You should carefully compare your short-term and long-term disability policies to ensure you understand the requirements of your long-term disability policy.

Transitioning from STD to LTD with Different Insurance Companies

Going from short-term disability to long-term disability can be more challenging for those whose LTD coverage is provided by a different insurance company than their STD coverage. This is because the new insurance company will not have immediate access to the medical records, reports, or other documentation that the claimant submitted in support of their short-term disability claim.

In these cases, claimants typically must submit a completely new claim, including claim forms from both the claimant and their treating physicians, as well as medical records. This process can be daunting. You should make sure you have copies of your short-term disability approval letter and any other documentation that supported your STD claim. Submitting documents such as an STD approval letter can help demonstrate to a new insurance company that you meet the definition of disability.

Contact the Long-Term Disability Legal Team at Chisholm Chisholm & Kilpatrick

At Chisholm Chisholm & Kilpatrick, our team of experienced attorneys and professionals have helped many clients successfully transition from short-term disability to long-term disability. We can help bolster your claim so that you receive the benefits to which you are entitled.

Our team is experienced with benefit limitations and can help ensure the insurance company does not incorrectly limit your benefits once you make the transition to long-term disability. Contact us today at (800) 544-9144 for a free consultation to see how we may help you.