Long-Term Disability (LTD) Claims for Psychologists

If you are currently suffering from a condition that prevents you from working as a psychologist, you have the option to file a claim with your insurance company for long-term disability (LTD) benefits. Read more to learn about what LTD insurance for psychologists entails and how to increase your chances of getting your claim approved.

Types of Psychologists

According to the Bureau of Labor Statistics (BLS), around 180,000 individuals are currently employed as psychologists in the United States. To become a psychologist, you usually need to obtain a license and a doctoral degree, although a master’s degree can be sufficient in some cases.

Psychologists can either work independently (e.g., conducting research or working one-on-one with clients) or work as part of a healthcare team (e.g., collaborating with other healthcare professionals or working in a school setting). As a psychologist, you are typically responsible for observing, interviewing, and diagnosing patients.

The following are some common types of psychologists:

Clinical psychologists – Clinical psychologists usually work directly with patients to treat and diagnose mental, emotional, and behavioral disorders. These can range from short-term crises to more severe, chronic conditions. Some psychologists focus on specific conditions (e.g., clinical depression) while others focus on a specific group of people (e.g., adolescents, families, minorities, etc.). Clinical psychologists use a variety of approaches to help their clients, including interviewing, diagnostic tests, therapy, and behavior modification programs.

Community psychologists – Community psychologists work in a variety of environments (e.g., government agencies, community organizations, universities) to research community mental health issues. They work to empower individuals to change negative circumstances, prevent future issues, and strengthen their communities. For example, a community psychologist may be involved in collaborating with schools to prevent bullying.

Developmental psychologists – Developmental psychologists study the psychological progress and development of humans throughout their lives.

Forensic psychologists – Forensic psychologists work within the criminal justice system to help analyze and understand the psychological background of cases. If a case goes to court, they may testify as an expert.

Industrial/organizational (I/O) psychologists – I/O psychologists specialize in improving productivity, employee morale, health, and the quality of work life. They conduct research and apply psychological principles to help organizations meet these goals. Some work as management consultants while others serve as human resources specialists.

Military psychologists – Military psychologists are either service members or independent contractors who work with patients in the military.

Being a psychologist requires specific skills and abilities, and it is a demanding and often stressful career. If you develop a certain condition or illness, it will undoubtedly affect your ability to work and perform the daily tasks of a psychologist.

Occupational Hazards for Psychologists

Working as a psychologist can be mentally and emotionally draining, which can lead some individuals to develop disabilities or exacerbate preexisting conditions. Conversely, the responsibilities and duties of a professional psychologist can be difficult to fulfill if you are suffering from a disability, even if its origin is unrelated to your profession.

If you are unable to meet certain expectations of the position, you may face occupational hazards, which can put your patient’s wellbeing or your own wellbeing at risk. Some occupational hazards faced by psychologists include:

- The challenge of managing intimate, confidential, and nonreciprocal relationships with clients

- The stress of working with people in distress

- The demands of clinical and professional responsibility

- Feeling isolated at work

- Aspects of the role that can lead to burnout (e.g., limited control over outcomes, limited resources, overinvolvement, poor boundaries)

- The difficulty of balancing stress from both a work and personal life

When ignored, these occupational hazards have potential consequences, including depression, social isolation, addictions, unprofessional behaviors, ethical violations, and stress-related illnesses. In turn, these consequences can have a negative and potentially dangerous effect on the well-being of clients.

Qualifying for Long-Term Disability (LTD) Benefits

Before filing an LTD claim, it is important to understand what coverage is available to you. There are typically two ways to obtain LTD coverage. You can either get LTD insurance through your employer as a work benefit (i.e., a group policy) or you can purchase it directly from an insurance company (i.e., an individual policy). As a psychologist, you may qualify for either option.

You can ask your employer for information regarding your employment benefits to determine if you have an employer-provided group policy. Your employer should provide you with the complete plan governing documents for each benefit plan you participate in, including long-term disability.

To determine if you have an individual LTD policy, you can review your financial records to see if there is evidence of premium payments to an insurance company. If you do find evidence of premium payments, you can request a copy of your policy from the insurance company.

Importance of Reading and Understanding Your LTD Policy

It is essential to read and understand the terms of your LTD policy to know what is needed to qualify for LTD benefits. Your LTD policy should include the definition of disability, deadlines you must meet, the maximum benefit period, limitations to your benefits, and other crucial information.

It may also be a good idea to read your policy thoroughly before you even need to file a claim. This will allow you to evaluate the coverage available to you in the event you become disabled, as well as inform you if purchasing additional coverage is necessary.

Definition of Disability and Material Evidence

One of the most important pieces of information that your long-term disability policy contains is the definition of disability. The definition of disability tells you the level of functional impairment you must meet to qualify for long-term disability benefits, what level of protection your policy provides, as well as what evidence you need to submit in support of your claim.

When filing a long-term disability claim, you must explain why you meet the applicable definition of disability and provide supporting evidence. Supporting evidence can include medical records, reports from your physicians, and statements from family, friends, or coworkers. Vocational evidence, or opinions from vocational experts, can also be useful in proving your claim.

“Own Occupation” vs. “Any Occupation”

There are two definitions of disability that you will typically find in most long-term disability policies: the “own occupation” definition and the “any occupation” definition. Some LTD policies transition from the “own occupation” to the “any occupation” after the claimant receives benefits for a certain number of months.

Own occupation – Focuses on whether you can perform the material duties of your specific profession, in this case, a psychologist. Material duties of a job include both physical and cognitive capabilities. For example, can you carry out complex tasks or concentrate? As a psychologist, can you manage responsibilities like interviewing and diagnosing clients or does your disability prevent you from doing so?

Any occupation – Focuses on whether you can perform the material duties of any occupation. Some “any occupation” definitions of disability include the gainful component. A gainful occupation would be one where you earn a certain percentage, usually 60 to 80 percent, of your pre-disability earnings.

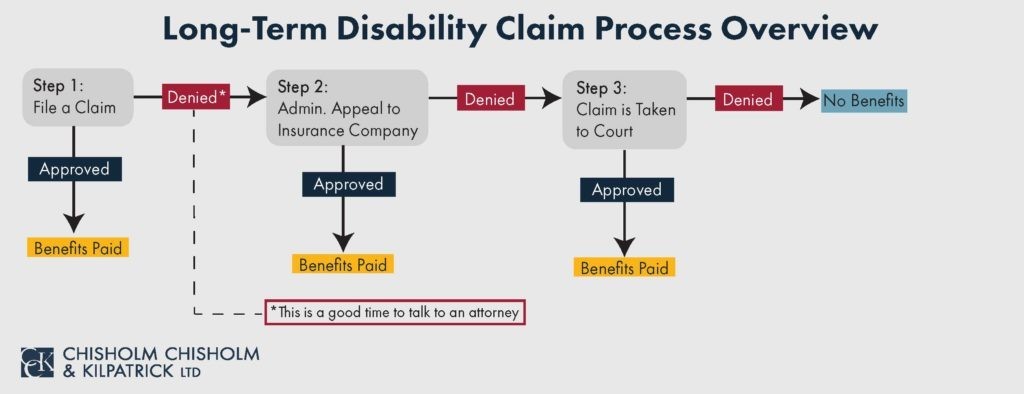

Was Your Long-Term Disability Claim Denied?

If your insurance company denied your claim for long-term disability insurance, Chisholm & Kilpatrick LTD may be able to help. CCK has extensive experience successfully helping individuals with initial claims, administrative appeals, or court litigation. Our LTD attorneys may be able to put our resources and experience to work for you.

Call CCK today to schedule a complimentary case review.