Long-Term Disability (LTD) Claims for Engineers

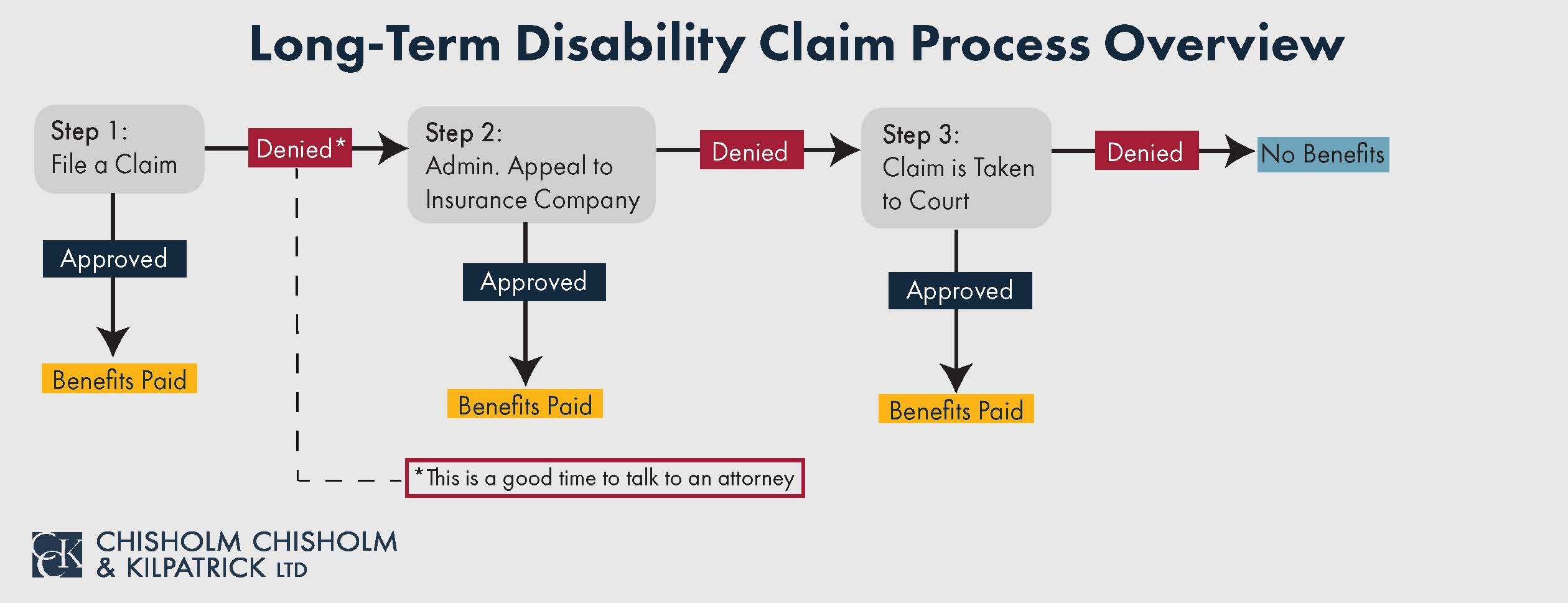

Long-term disability (LTD) insurance coverage can help protect a percentage of a person’s pre-disability earnings when they develop a medical condition (physical or mental) that prevents them from working. Engineers are highly skilled individuals, and when they become unable to work they may require these monthly benefits. However, obtaining these benefits is often challenging because insurance companies routinely deny disability claims. When a disability insurance company denies a claim for benefits, it can seem a difficult obstacle to overcome, but engineers have the right to appeal this decision.

This article will discuss long-term disability claims for individuals who work in the engineering field, and answer some of the questions you may have as an engineer who needs to file a long-term disability claim.

The Occupational Duties of Engineers

Engineering is a complex field that requires strong cognitive abilities, such as excellent reasoning and analytical skills. It is a profession that uses practical applications of scientific and mathematical methods to design technological solutions for the developing world. When engineers cannot perform their occupational duties, then mistakes are liable to happen. This not only affects their own work but the work of their colleagues too.

While the day-to-day specifics of engineering jobs may differ, they all require some of the same fundamental competencies and skills, including logic and problem-solving abilities; excellent analytical skills; a lifelong desire to learn; attention to detail; creativity; innovation; and strong communication skills. Engineers must also be comfortable working in a highly competitive and constantly changing field and be able to handle stressful or high-pressure situations. Unfortunately, given these requirements, even a mildly impairing condition can impact your ability to perform your occupation as an engineer.

Types of Engineers

Though there are numerous specialized fields of engineering ranging from biomedical to aerospace, engineers can typically be divided into four major categories: chemical, civil, electrical, and mechanical.

- Chemical engineers apply math, chemistry, physics, and biology to change raw materials into more practical and useful forms. The term “chemical engineer” may apply from anyone working on immunology and genetic engineering to someone who uses molecules and materials to create everything from Silly Putty to Kevlar.

- Civil engineers can be broken out into six major subcategories: environmental, geotechnical, structural, transport/transportation, utility, and water resources. Civil engineers are responsible for analyzing survey reports, maps, and other data to determine the best locations for everything from water supply networks to shopping malls; performing or overseeing surveying and building operations; conducting risk analysis and developing cost estimates; and utilizing computer design software to develop complex projects such as transportation systems.

- Electrical engineers manage the analysis and application of electricity, electronics, and electromagnetism. Their duties include designing, testing, and supervising the manufacture and installation of electric equipment or electronic systems.

- Mechanical engineers are responsible for the design and operation of various machines and mechanical systems. This type of engineer may develop telescopes and cameras; create and test sports equipment; design automotive, naval, aerospace, and marine vehicles; or construct and maintain power plants and energy efficiency systems.

- Other types of engineers that fall into more than one category include nuclear, biomedical, aerospace, industrial, agricultural, and more.

No matter what type of engineer you are, it is likely that your work is challenging and demanding. However, if you develop a medical condition that limits your ability to perform the duties of your job, it is important to know your options regarding long-term disability coverage.

Two Types of Long-Term Disability Policies

The first step to understanding long-term disability (LTD) benefits is to read your long-term disability policy thoroughly. It is important to do this before you become disabled and need to file a claim so that in the event you develop a disabling condition, you will understand the coverage available to you. These policies contain a myriad of vital information, such as the definition of disability; how to file a long-term disability claim with your insurer; how to appeal a long-term disability claim denial; and more.

This coverage is generally broken down into two different types of long-term disability policies: individual and employer-provided group policies. An individual policy is one purchased directly from an insurance company by an individual and is separate from any company-sponsored benefits you might have. An employer-provided group policy is offered through your job as a benefit of employment. ERISA, a strict federal law, governs most group policies. If you are unsure which type of policy you have, there are a few things you can do.

How to Determine What Type of LTD Policy You Have

To determine if you have a group policy, you should inquire with your employer or company’s Human Resources department about the benefits available to you. You can also review your pay stubs to see if a premium for an employer-provided group policy was deducted from your paycheck to be paid to an insurance company. However, some employers pay the full premium for their employees, so you may still have group long-term disability coverage even if you do not see any premium deductions on your paystubs. If you believe you have an individual policy, you should review your regular bank statements to see if you paid a premium to an insurance company, as premiums for individual policies are not likely to appear on pay stubs.

In both instances, you will want to request a copy of your disability policy so that you can familiarize yourself with the elements of your specific coverage. Your policy will also contain key details such as any potential limitations that may apply; important deadlines the maximum benefit period; and more.

Establishing a Claim for Long-Term Disability Benefits as an Engineer

In order to establish your eligibility for long-term disability benefits, you must first prove that you meet the definition of disability as outlined in your policy. The definition of disability is a crucial element of your long-term disability policy, as it determines the level of impairment you need to meet to receive benefits. Long-term disability policies typically reference two main definitions of disability — own occupation and any occupation — although the language and specifics can vary, which is why it is always important to carefully review your policy.

Own Occupation vs. Any Occupation Definitions of Disability

The own occupation definition of disability considers whether you can perform the material duties, both physical and cognitive, of the job you were doing at the time you became disabled. This definition of disability usually considers how your occupation is performed on average nationally, as opposed to how it is performed for your specific employer.

The any occupation definition of disability asks if you can perform the material duties of any occupation, not just your own, reliably and consistently. Sometimes this definition also includes a gainful component, meaning it asks whether you can perform the material duties of any gainful occupation. A gainful occupation is one in which you could earn a percentage (typically 60 to 80 percent) of your pre-disability earnings.

The Definition of Disability May Change

It is important to note that the definition of disability usually changes after a certain period, typically 24 or 36 months of benefits. When you first become disabled, you will likely have to meet an own occupation definition of disability through the elimination period and, most commonly, the first 24 months of benefits.

Following the own occupation period, the definition of disability will likely change to any occupation, at which point the insurance company will conduct a review to ensure you meet the new definition of disability. Often, claimants who were working as engineers at the time they became disabled have an easier time meeting the own occupation definition of disability than the any occupation definition.

How Engineers Can Prove That Their Medical Condition Meets Your Policy’s Definition of Disability

There are several ways in which you can prove that you meet the applicable definition of disability and are therefore eligible to receive long-term disability benefits. Medical evidence in the form of treatment records and medical history, medications being taken, or statements from your doctor detailing your condition can be particularly useful in building a case for long-term disability benefits.

Additionally, statements from your family, friends, and co-workers can help paint a fuller picture of your condition and the way it impacts the daily activities required in your job and your life. In some instances, opinions from vocational experts can also serve as beneficial pieces of evidence.

How Can a Disability Impact My Career as an Engineer?

Even the mildest condition or disability may have a significant impact on, or prohibit you from performing, the daily duties of an engineer. For example, if you are a mechanical engineer and develop a hearing condition that leaves you extra sensitive to sound, you may find yourself unable to operate or oversee the types of loud machinery necessary to develop and test automotive vehicles.

As an electrical engineer who had a pacemaker installed as the result of a heart condition, you may be unable to continue work at certain job sites where magnets or strong electrical fields could adversely affect your pacemaker and potentially even lead to heart complications.

Alternatively, as a chemical engineer working with toxic substances, you may develop chronic migraines that impair your ability to concentrate and pay attention to small details. Additional symptoms of migraines, including nausea and lack of sleep, could lead to you making more mistakes and becoming a less-effective worker, as well as potentially jeopardizing your own safety and the safety of your co-workers. As these symptoms are often frustrating, you could also develop a poor temperament that may negatively impact your professional and personal relationships.

Similarly, you may be a civil engineer suffering from back pain that causes frequent discomfort and impacts your ability to focus. Although you may take medication to manage your symptoms, the medication might further decrease your ability to focus, resulting in your inability to do fieldwork. You may have to avoid job sites with uneven ground, heights, and other potentially dangerous situations that require a high level of concentration.

How Do Insurance Companies Pay Claimants Their Benefits?

Depending on the specifics of your policy, the insurance company will either pay you a fixed monthly benefit regardless of your “pre-disability earnings,” or it will take a percentage of your pre-disability earnings to determine your monthly benefit. Certain policies take the average amount you earned over a period of years before becoming disabled in order to determine your pre-disability earnings — as in the case of an hourly employee who did not work the same regular number of hours each week or an employee whose pre-disability earnings included commissions that varied over time — while others may only consider your annual salary as of the last day you worked prior to your disability.

As an engineer, you likely received a steady salary based on your position and experience level, which means that your income probably did not vary drastically from year to year, except in the case of a promotion or raise, so your monthly disability benefit would be about the same, regardless of how your policy defines pre-disability earnings.

Can Engineers Return to Work While Receiving LTD Benefits?

It is also possible that your long-term disability policy will allow you to work in some capacity and still receive benefits, meaning you could receive a portion of your monthly benefit, typically based on the loss of income between your pre-disability earnings and current work earnings.

Your pre-disability earnings will help determine both the amount of your monthly benefit under the partial disability provisions as well as how much you are able to earn while still maintaining eligibility for your disability benefits. However, as each policy is different, it is crucial that you thoroughly read your specific policy to understand all your options.

What Is a “Gainful Component” Present in Some Long-Term Disability Policies?

Additionally, as discussed above, some long-term disability policies include a gainful component under the any occupation definition of disability. The any occupation definition is often harder for claimants to meet, especially if they had a particularly physically or mentally demanding job prior to becoming disabled. For example, a condition that prevents you from being an engineer may not impact your ability to perform another, less demanding occupation.

However, the any occupation definition can be easier to meet if your policy includes a gainful component. If your pre-disability earnings were high, then the gainful component is likely to equate to a high amount as well, and a higher salary often indicates a more challenging job. As a result, if your medical condition prevents you from working as an engineer and other similarly challenging occupations, then you may still receive disability benefits due to your policy’s gainful component (even though you are able to perform other, less challenging occupations). Again, you should review your long-term disability policy in its entirety to determine the unique components of your long-term disability coverage.

What About Social Security Benefits for Engineers?

Social Security Disability Insurance (SSDI) benefits may also be available to you, in addition to your long-term disability benefits. SSDI typically applies when a person is unable to engage in any substantial, gainful activity, and their disability will last at least 12 months or result in death, although there are many other rules that also apply to these types of claims.

However, it is important to note that the SSDI definition of disability is often very different than the definition of disability in your long-term disability policy. This means that you may be granted disability benefits through your long-term disability policy and denied benefits through SSDI; a grant of one type of benefit does not automatically mean you will be granted another type, regardless of how similar the two may seem to you.

Call CCK Today for a Free Case Evaluation

We know that every situation is different. Chisholm Chisholm & Kilpatrick has been helping long-term disability claimants for over 20 years. Receiving benefits for a medical condition that is limiting your ability to work as an engineer can be frustrating, but this is not a process that you must handle on your own. If your insurance carrier denies your claim, then you have the right to appeal. CCK can help you understand your coverage. We want you to begin receiving your long-term disability insurance benefits.

By considering every available piece of evidence, from your specific health issues to the day-to-day responsibilities of your specific job to objective medical evidence regarding your condition, we connect the details of your case in a way that leaves no questions unanswered. Our team explores every avenue in order to develop strong disability claims and help our clients obtain the benefits they need. Call CCK today at (800) 544-9144 for a free case evaluation with a member of our team. We will analyze your case and determine if we can assist you.

Share this Graphic